The most dangerous part of a construction loan starts after approval.

Every draw request creates another funding decision. Another inspection. Another document review. Another opportunity for delays, fraud, or money to be released before work is actually completed.

That is what makes construction loan servicing fundamentally different from traditional mortgage servicing, especially for private and hard money lenders managing projects across the US and Canada. Funds move in stages, disbursements depend on construction milestones, and risk continues to change throughout the life of the project.

For lenders managing multiple active projects at once, manual tracking quickly becomes difficult to control. Draw approvals, inspections, contractor invoices, compliance records, and payment schedules all have to stay synchronized across the portfolio.

As a result, construction loan servicing is increasingly shifting toward centralized software and automation systems that help lenders reduce operational risk, improve visibility, and scale construction lending workflows more consistently.

What Is Construction Loan Servicing?

Construction loan servicing refers to the ongoing management of a construction-stage loan after origination and throughout the building process. The Consumer Financial Protection Bureau describes construction loans as shorter-term loans where funds are disbursed in stages, often based on project progress and inspections.

In practice, that means the lender stays involved throughout the build. Every draw request has to be reviewed. Inspections have to confirm completed work. Disbursements have to match actual project progress. Documentation, contractor communication, interest tracking, and compliance records all continue accumulating while the project is still under construction.

The servicing process is really about controlling risk while capital moves through an unfinished project. That is why construction loan servicing very quickly becomes operationally heavier than standard mortgage servicing.

Why Construction Loan Servicing Is More Complex Than Traditional Lending

Traditional mortgage lending usually follows a straightforward servicing structure after closing. Construction lending does not. Funds are released in multiple stages throughout the project, which means lenders continue making servicing and risk decisions long after the loan has been approved.

Each draw cycle often depends on inspection-based approvals, contractor payment verification, updated project documentation, and confirmation that construction milestones have actually been completed before additional funds are disbursed.

That complexity also creates higher fraud exposure. Duplicate invoices, inflated draw requests, incomplete work, and unauthorized contractor activity can become difficult to detect when servicing workflows rely heavily on manual oversight.

At the same time, construction projects frequently change during development. Revised timelines, budget adjustments, change orders, and evolving compliance requirements all create additional reporting and operational pressure that traditional mortgage servicing workflows are not designed to handle consistently at scale.

How Construction Loan Servicing Software Works

Construction loan servicing software helps lenders centralize the operational side of managing active construction projects after closing. Instead of tracking draw activity, inspections, disbursements, and project documentation across spreadsheets, emails, and disconnected systems, lenders can manage servicing workflows through a single, centralized platform.

Most construction loan servicing platforms include centralized loan dashboards that give servicing teams visibility into active projects, outstanding draw requests, inspection status, payment activity, and remaining loan balances across the portfolio.

Automated draw request workflows help standardize how funding requests are submitted, reviewed, approved, and disbursed. Many systems also integrate inspection tracking and document verification workflows so lenders can validate construction progress and supporting documentation before releasing funds.

As portfolio volume grows, real-time visibility becomes more difficult to manage manually. Construction loan software for private lenders in CA and the US helps servicing teams keep inspections, draw activity, disbursements, and project documentation connected across all active construction portfolios.

Key Workflows of Construction Loan Management

Construction lending becomes harder to manage when multiple projects, draw requests, inspections, approvals, and disbursement schedules are moving simultaneously. Lenders need a clear process for keeping those activities connected, even when some steps are handled by internal teams, inspectors, contractors, or third-party providers.

Strong construction loan management usually depends on workflows that support:

- Draw request management: A consistent process for submitting, reviewing, approving, and recording draw requests throughout the construction lifecycle.

- Inspection and milestone coordination: A clear way to track inspection status, project milestones, approval dependencies, and supporting documentation before funds are released.

- Portfolio visibility: A clear way to monitor active projects, outstanding draws, loan balances, payment activity, and servicing status across the portfolio.

- Risk review and verification steps: Processes that help lenders review borrower information, supporting documents, invoices, approvals, and funding activity before each disbursement decision.

- Construction document management: A central place to organize inspection reports, contractor records, compliance files, draw documentation, and other project-related materials.

- Payment and disbursement scheduling: Workflows for managing interest payments, draw disbursements, repayment activity, and timing requirements throughout the project.

- Compliance and audit records: Reliable records of approvals, documentation, funding decisions, and servicing activity to support internal reviews and regulatory requirements.

How to Streamline Construction Loan Servicing

Construction loan servicing often becomes difficult to scale because too many operational decisions continue happening after the loan closes. Every draw request, inspection update, contractor invoice, and disbursement approval adds another layer of coordination that servicing teams have to manage accurately and in the correct order.

Many lenders streamline construction loan servicing by automating the parts of the workflow that create the most operational friction. For example, draw approval workflows can be standardized so funding requests move through consistent review processes instead of relying heavily on back-and-forth communication between servicing teams, inspectors, contractors, and borrowers.

Inspection workflows can also be centralized inside the servicing platform, giving teams clearer visibility into which projects are awaiting inspections, pending approval, or missing supporting documentation before additional funds are released.

Modern loan servicing software for private lenders also helps consolidate project documentation, accounting activity, draw histories, and reporting workflows into a single environment. Real-time servicing dashboards then make it easier to monitor project status, outstanding disbursements, and portfolio exposure across active construction loans without relying on fragmented manual tracking processes.

How to Reduce Construction Loan Fraud Risk

Construction lending creates more fraud exposure than traditional mortgage servicing because funds are released gradually throughout the project rather than all at once at closing. Every draw request introduces another opportunity for inaccurate invoices, incomplete work claims, duplicate documentation, or unauthorized disbursement activity if servicing controls are not tightly managed.

A 2025 analysis of construction fraud and mismanagement estimates that fraud and mismanagement together can account for up to 10% of total construction costs. In the U.S. alone, that represents tens of billions of dollars in annual losses.

Many lenders reduce construction loan fraud risk by building stricter validation workflows directly into the servicing process. Inspection verification is often one of the first control layers, helping lenders confirm that construction milestones have actually been completed before additional funds are released.

Controlled draw release rules add another layer of oversight by limiting when disbursements can move forward and what approvals or documentation are required first. Multi-step approval systems also help reduce the likelihood of a single servicing decision triggering an unauthorized release of funds.

Pricing Comparison in Construction Loan Management SaaS

Pricing isn't just about the monthly software cost. For construction lenders, the real comparison is between the cost of a platform and the cost of continuing to manage draws, inspections, disbursements, and reporting manually.

The most common pricing models include:

- Subscription-based pricing: A recurring monthly or annual fee, often based on users, features, servicing volume, or platform access.

- Per-loan pricing: A model where pricing is tied to the number of active loans being managed. This usually works best for smaller construction portfolios or lenders with lower, more predictable volume.

- Portfolio-based pricing: A model based on overall portfolio size, servicing activity, or broader platform usage. This can be more practical for lenders managing many active projects at once, especially when per-loan pricing starts to penalize growth.

Beyond the pricing model itself, lenders should also compare implementation costs, integration work, maintenance needs, and the cost of manual servicing. Manual processes may look cheaper upfront, but the long-term cost often shows up in staff time, delayed approvals, reporting gaps, and limited visibility across active construction loans.

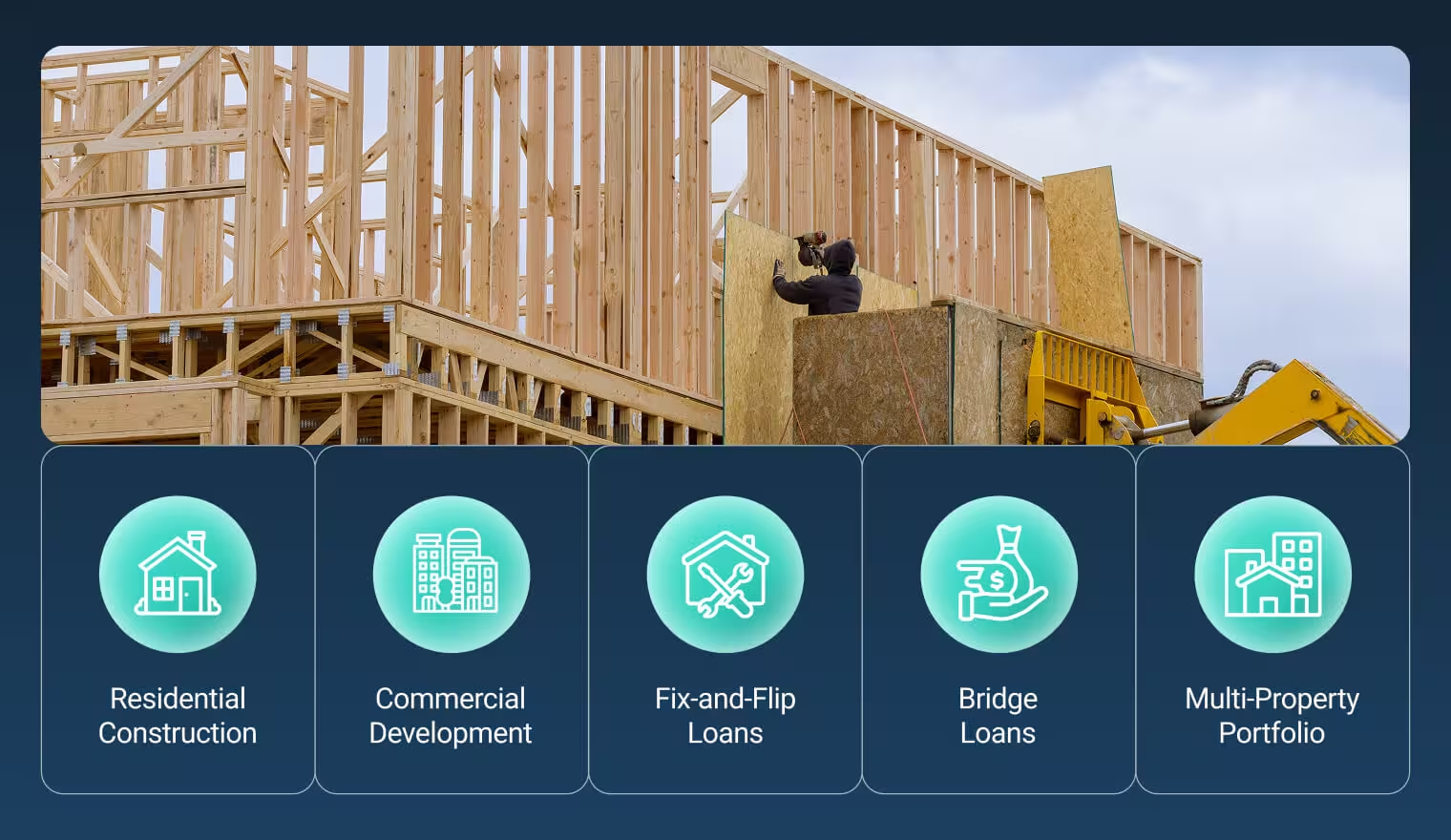

Use Cases for Private and Hard Money Lenders

Construction servicing does not look the same across every deal. A ground-up build, a commercial development, a fix-and-flip, and a multi-property portfolio all create different draw patterns, inspection needs, and timing pressure.

This becomes clear when you look at what servicing teams actually have to manage:

- Residential construction lending: Ground-up residential projects often involve multiple draw stages tied to visible construction progress. Servicing teams need a clear way to track inspections, borrower updates, contractor invoices, and remaining funds without losing control between milestones.

- Commercial development financing: Larger commercial projects can create a longer paper trail with more stakeholders involved at every stage. Servicing workflows help lenders keep draw approvals, contractor records, inspection results, and disbursement history connected before small gaps turn into expensive ones.

- Fix-and-flip loans: Fix-and-flip loans depend on tight coordination between renovation progress, draw approvals, and exit timing. Servicing teams need visibility into what has been completed, what has been funded, and what still needs review.

- Bridge construction loans: Bridge construction loans often sit inside a narrow window where delays can affect the borrower’s next financing step. Servicing teams need clear visibility into what has been funded, what still needs inspection, and whether the project is still aligned with the expected repayment timeline.

- Multi-property portfolios: Once several construction loans are active at the same time, individual project tracking is no longer enough. Lenders need a portfolio-level view of outstanding draws, inspection status, released funds, and project risk so small issues do not disappear inside a larger book of loans.

Future of Construction Loan Servicing

AI tools are beginning to play a larger role in how lenders review draw requests and monitor funding activity throughout the project lifecycle. Instead of waiting for a servicing team to catch every missing document, duplicate invoice, or unusual request manually, software can help flag issues before a draw moves forward.

Real-time construction monitoring will push that further. Site updates, inspection data, photos, and connected project tools can give lenders a clearer view of progress between formal inspections.

Predictive risk modeling adds another layer by helping lenders spot projects that may be drifting off schedule, exceeding budget, or showing early signs of repayment risk.

Automated compliance reporting will also reduce the amount of time teams spend pulling together approval histories, inspection records, and disbursement documentation after the fact.

The next step is more connected servicing systems: construction loan servicing is moving toward more autonomous platforms where draw activity, inspections, compliance, and portfolio risk are tracked in real time instead of pieced together manually after problems appear.

Final Thoughts

Construction lending does not slow down once the loan closes. In many ways, that is when the operational pressure actually begins.

Every active project creates a constant stream of inspections, draw requests, approvals, invoices, timeline changes, and servicing decisions that all need to stay aligned as funds move through the project.

That becomes much harder to manage manually as portfolios grow.

The lenders gaining the most control over construction servicing are usually the ones building more structure around those workflows early, before operational gaps start affecting approvals, visibility, or project risk.

If your team is still managing construction draws manually, book a demo with Mortgage Automator to see how construction loan software can bring more control to every draw, inspection, and funding decision.

Frequently Asked Questions

What is construction loan servicing?

Construction loan servicing is what happens after approval, when the lender still has to control how funds move through the project. It covers draw reviews, inspections, disbursements, contractor updates, and the records needed to prove each release of capital was justified.

How does construction loan servicing differ from traditional mortgage servicing?

A traditional mortgage usually follows a predictable repayment structure after closing. Construction loans are different because funding is released in stages, which means lenders continue making servicing decisions throughout the build.

What are the biggest challenges in managing construction loans?

Managing construction loans becomes challenging when draw requests, inspections, invoices, approvals, and project updates start moving simultaneously across several active loans. Keeping those workflows organized manually can become difficult very quickly.

How can private lenders streamline construction loan servicing?

Many private lenders streamline construction loan servicing by automating draw approvals, centralizing inspections and documentation, and using real-time dashboards to monitor project activity across the portfolio instead of relying on spreadsheets and email chains.

What features should construction loan management software include?

The strongest construction lending platforms usually combine draw approvals, inspection coordination, contractor documentation, reporting, and portfolio monitoring within one servicing system so lenders can manage projects without relying on disconnected tools.

How can lenders reduce construction loan fraud risk?

The strongest fraud controls are built into the servicing workflow itself: verified inspections, authenticated documents, controlled draw releases, and records that show who approved what, when, and why.

What is portfolio management software for construction loans?

Instead of tracking each construction project separately, portfolio management software for construction loans gives lenders one place to monitor funding activity, inspection progress, outstanding draws, and servicing status across multiple active loans.

What are draw management workflows in construction lending?

In construction lending, draw management workflows help control how and when funds move during the build. Each draw request typically passes through inspections, supporting documentation checks, and approval stages before additional capital is released.

How does construction loan software help hard money lenders?

Hard money lenders often use construction loan software to keep funding decisions, inspections, contractor documentation, and servicing records connected throughout the project lifecycle instead of managing each step separately.

What should private lenders look for in construction loan software in Canada and the US?

Private lenders in Canada and the US should look for construction loan software that supports draw automation, inspection workflows, fraud controls, compliance tracking, and portfolio-level visibility across active projects.