Many private lenders begin with spreadsheets because they are easy to build, inexpensive to manage, and flexible enough for a small portfolio.

At first, that can work well. A simple loan servicing spreadsheet can track borrower details, payment dates, balances, notes, and basic reporting without adding a new platform to the business.

The problem is that spreadsheets become harder to trust as loan volume grows. More loans mean more payment schedules, more calculations, more borrower records, and more chances for something to be missed.

That is why many lenders eventually look for alternatives to spreadsheet-based loan servicing. The goal is not just to replace a spreadsheet; it is to move into a more reliable servicing process that supports growth, reduces manual work, and gives teams better control over the portfolio.

Why Private Lenders Still Start with Spreadsheets

Spreadsheets are not the problem at the beginning. For many private lenders, they are a practical starting point.

They are useful because they are:

- Low cost: Teams can start tracking loans without investing in software right away.

- Familiar: Most operators already know how to use spreadsheets.

- Flexible: Lenders can add columns, formulas, tabs, and notes as needed.

- Fast to set up: A basic servicing tracker can be created quickly.

- Good for simple portfolios: When there are only a few loans, manual tracking can still feel manageable.

That flexibility is exactly why many lenders rely on spreadsheets longer than they should. But a spreadsheet only records information. It does not actively manage the servicing process.

It will not automatically:

- Flag missed payments

- Prevent duplicate records

- Maintain a reliable audit trail

- Send borrower reminders

- Reconcile payments

- Update reports in real time

- Give borrowers online access to loan information

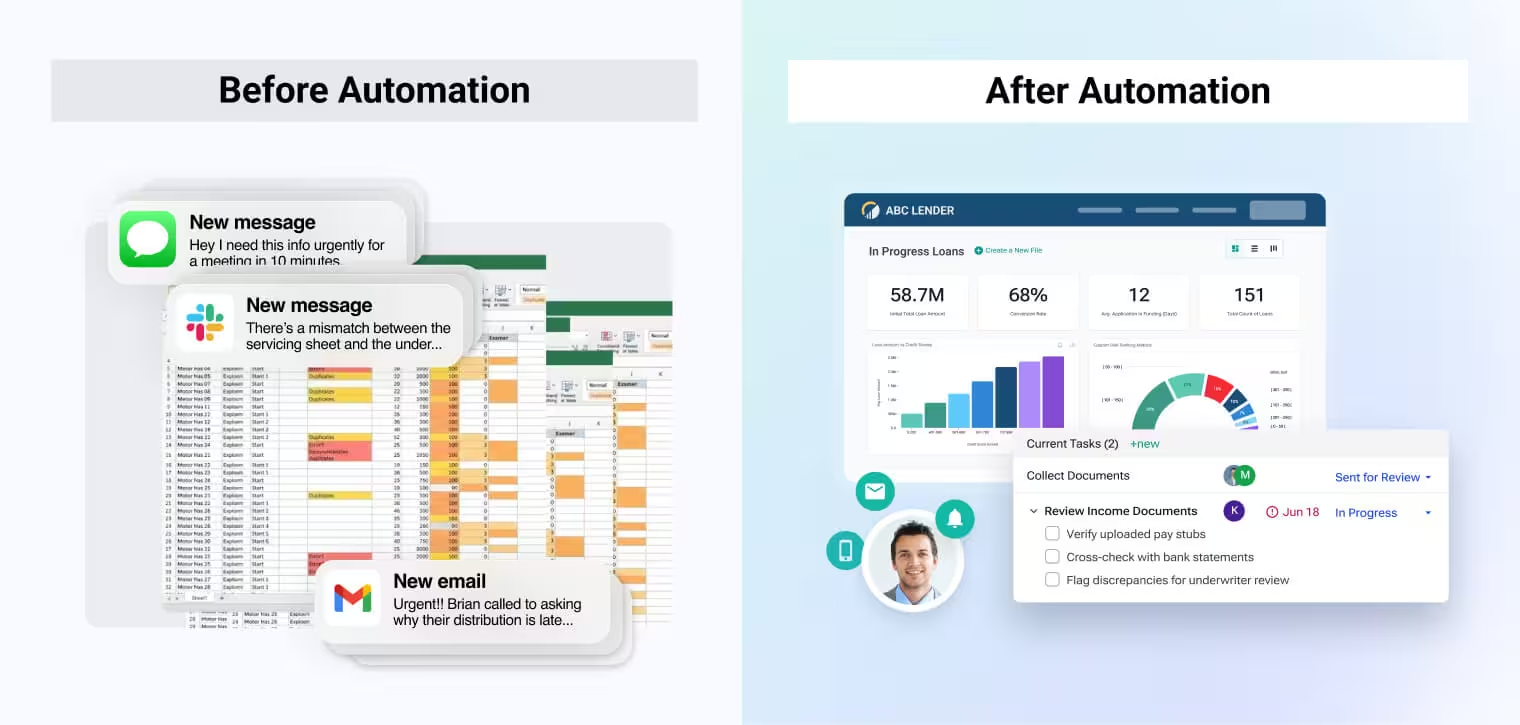

And as the portfolio grows, the loan servicing spreadsheet model becomes less of a helpful tracker and more of an operational risk. In fact, the European Spreadsheet Risks Interest Group and treasury practitioners report that almost 90% of spreadsheets contain some form of error, making them unreliable as complexity grows.

Hidden Costs of Spreadsheet-Based Loan Servicing

Spreadsheets look inexpensive on the surface. The hidden cost comes from the manual work around them.

Common issues include:

- Manual errors: Payment amounts, due dates, balances, and borrower details need to be entered by hand.

- Broken formulas: One edited or copied formula can affect interest calculations, balances, or reports.

- Missed due dates: Teams may rely on calendar reminders, manual checks, or memory.

- Duplicate records: Borrower and loan details can be repeated across tabs, files, or folders.

- Slow reporting: Reports often require cleanup before they can be shared with leadership, investors, or auditors.

- Compliance exposure: Servicing records may be scattered across spreadsheets, emails, PDFs, and internal notes.

- Chargeback issues: Payment disputes become harder to investigate when the full servicing record is not centralized.

These problems usually build gradually. A lender may not notice the risk when there are 10 active loans. At 40, 60, or 100 active loans, the same process can start slowing everything down.

That is often when lenders begin looking for software to reduce servicing errors and chargebacks. Ultimately, the goal is to make servicing more accurate, visible, and consistent.

.avif)

Signs You’ve Outgrown Spreadsheet Loan Servicing

A loan servicing spreadsheet does not fail all at once. The warning signs usually appear across the servicing process:

- You are managing 25–50+ active loans

At this stage, there are more borrowers, more due dates, more payment exceptions, and more reporting that needs to be managed manually.

- Payment reconciliation is manual

If your team is still matching payments, updating balances, checking exceptions, and confirming transactions by hand, servicing will become harder to scale.

- Reporting takes hours

Reports should help the business make faster decisions. If the team has to clean spreadsheet data every time a report is needed, the process is already slowing the operation down.

- Chargebacks are increasing

More chargebacks can point to gaps in payment tracking, borrower communication, authorization records, or reconciliation.

- Compliance documentation is messy

If records are spread across spreadsheets, inboxes, shared drives, and manual notes, it becomes harder to prove what happened and when.

- Team collaboration is inefficient

When multiple people work from the same spreadsheet, version control becomes a risk. Teams may not know which file is current or who owns each update.

- Borrowers expect online payments

Borrowers increasingly expect digital access to payments, balances, statements, and updates. A spreadsheet cannot provide that experience on its own.

7 Best Alternatives to Spreadsheet-Based Loan Servicing

The right platform depends on the lender’s size, workflow, team structure, and growth plans.

For this comparison, the main evaluation criteria are:

- Servicing automation

- Borrower experience

- Payment tracking

- Reporting

- Scalability

- Compliance support

- Fit for private lending operations

1. Mortgage Automator

Best for: Private lenders looking for an all-in-one loan origination & servicing software

Mortgage Automator is the best fit for lenders whose servicing process has started to depend too much on reminders, manual checking, and spreadsheets. Once payment changes, borrower updates, investor details, and exceptions are spread across different files, teams spend more time checking the record than using it.

That makes it a strong choice for lenders planning to scale. Mortgage Automator supports automated payment handling, ACH/PAD, payment tracking, NSF tracking, borrower and investor statements, servicing reports, and accounting-related reports, while keeping servicing connected to origination, portals, documents, and fund management.

Key strengths:

- Flexible payment schedules and automated ACH/PAD payments

- Payment tracking with borrower notifications

- Borrower and investor statements

- Servicing reports and dashboards

- Audit-friendly workflows for compliance and recordkeeping

Why it works for scaling lenders:

- It connects origination and servicing

- It reduces duplicate data entry

- It improves visibility across the entire loan lifecycle

Potential limitation:

Mortgage Automator works best when teams have time to set up their servicing workflows properly. Lenders moving from loan servicing spreadsheets should allow time for onboarding so they can get the full value from the platform.

2. LoanPro

Best for: API-first servicing and customization

LoanPro is a good fit for lenders that need a highly flexible servicing platform with strong API and integration capabilities.

Key strengths:

- API-first servicing

- Payment automation

- Configurable workflows

Potential limitation:

Smaller teams may need more technical support during setup.

3. The Mortgage Office

Best for: Established private lenders managing diverse portfolios

The Mortgage Office is built for lenders that need servicing, accounting, reporting, and investor management tools in one system.

Key strengths:

- Servicing and accounting tools

- Investor management

- Reporting

Potential limitation:

The platform is strong in servicing and accounting, but lenders looking for a modern user experience and more automated workflows may find it less appealing.

4. Nortridge

Best for: Lenders with complex servicing requirements

Nortridge works well for lenders that need detailed servicing controls and flexible workflow configuration across different loan products.

Key strengths:

- Workflow configuration

- Payment processing

- Compliance tools

Potential limitation:

The setup process may feel complex for smaller teams moving directly from loan servicing spreadsheets.

5. TurnKey Lender

Best for: Digital lending automation

TurnKey Lender is a broader lending automation platform for teams that want origination, servicing, decisioning, payments, and borrower experience tools connected.

Key strengths:

- Lending automation

- Borrower portals

- Analytics and reporting

Potential limitation:

It may offer more functionality than smaller private lenders need at the current stage.

6. Bryt Software

Best for: Small to mid-sized private lenders

Bryt Software is a practical option for lenders that want to move away from spreadsheets without starting with a highly complex enterprise platform.

Key strengths:

- Loan management

- Payment tracking

- Borrower management

Potential limitation:

It may not offer the same depth of end-to-end private lending functionality as larger platforms.

7. LendFoundry

Best for: End-to-end lending lifecycle management

LendFoundry takes a broader approach than a standalone servicing tool, giving lenders a way to manage servicing alongside origination, payments, borrower communication, and reporting.

Key strengths:

- Origination and servicing support

- Payment automation

- Workflow automation

Potential limitation:

Implementation may be heavier than needed for lenders looking for a simpler spreadsheet replacement.

Comparison Table of Spreadsheet Alternatives

Features Small Lenders Should Prioritize

Small lenders do not need every feature on the market; they need the features that remove their biggest servicing risks.

The most important features to look out for include:

- Automated payment tracking: Helps reduce missed updates and manual reconciliation work.

- ACH/PAD and autopay: Makes repayment more consistent and reduces reliance on manual payment collection.

- Borrower portals: Gives borrowers access to balances, payments, documents, and updates without constant back-and-forth.

- Reporting dashboards: Helps teams monitor loan activity, portfolio performance, and servicing issues faster.

- Investor reporting: Makes it easier to share accurate portfolio and loan performance information.

- Audit logs: Creates a clearer record of servicing activity, user actions, payments, and changes.

- Compliance tracking: Helps teams keep required documents, actions, and records organized.

- Portfolio analytics: Gives lenders better visibility into trends, risk, repayment behavior, and growth.

- Payment reconciliation tools: Reduces the manual work involved in matching payments and resolving exceptions.

- Alerts and notifications: Keeps teams aware of upcoming due dates, missed payments, exceptions, and borrower activity.

How to Choose the Right Mortgage Loan Servicing Software for Small Lenders

Choosing mortgage loan servicing software for small lenders should start with an analysis of how the business actually works.

A good evaluation process should include the following considerations:

- Portfolio size: A tool that works for 10 active loans may start to break down at 50. Look at where your portfolio is now, but choose based on where it is heading.

- Loan complexity: Simple repayment schedules are one thing. Multiple loan types, investors, fees, draws, renewals, and exceptions need a system that can handle more moving parts.

- Team size: If one person owns servicing, the priority may be reducing admin work. If several people touch the file, you’ll need clearer permissions, workflows, and accountability.

- Growth plans: The right platform should give you room to add loans, users, reports, and workflows without forcing another operational rebuild too soon.

- Compliance requirements: Servicing records should be easy to find, verify, and report on. Look for audit trails, document tracking, and clear records of payment and borrower activity.

- Borrower expectations: If borrowers are asking for online payments, statements, or status updates, the servicing platform should make those interactions easier to manage.

- Budget: Spreadsheets may seem inexpensive, but the real cost shows up in manual work, reporting delays, servicing errors, chargebacks, and time spent fixing records.

The best choice is the one that removes the current bottlenecks without creating another system that the team will outgrow too quickly.

When to Move from Spreadsheets to Software

The best time to move is before spreadsheet issues start affecting borrowers, investors, or compliance.

Lenders often reach that point when:

- The portfolio is growing: More loans create more payment schedules, borrower records, and reporting needs.

- The team is expanding: Once multiple people are involved in servicing, version control becomes harder to manage.

- Compliance is becoming more complex: Servicing records need to be easier to find, verify, and share.

- Operational bottlenecks are slowing the team down: Reconciliation, reporting, and borrower updates start taking more time than they should.

- Borrowers expect digital servicing: Online payments, account access, and clearer communication are becoming standard expectations.

- Payment exceptions are increasing: Missed payments, chargebacks, failed payments, and manual corrections become harder to manage without a centralised system.

The move to software should make servicing easier to manage as the portfolio grows, especially when payment activity, reporting, and borrower communication become harder to track manually.

Future of Loan Servicing for Small Lenders

Loan servicing is becoming more automated, connected, and borrower-facing.

Key trends to watch include:

- Embedded payments: ACH/PAD, autopay, and integrated payment processing will make repayment easier to manage from inside the servicing system, with fewer manual updates after each transaction.

- AI servicing assistants: AI tools will help teams answer borrower questions, summarize loan activity, surface missing information, and spot servicing issues faster.

- Predictive delinquency alerts: Payment and portfolio data will give lenders earlier warning signs when a loan may need attention, helping teams act before a missed payment becomes a larger servicing issue.

- Automated collections: Reminder sequences, late notices, fee rules, follow-ups, and repayment workflows will become easier to manage consistently across the portfolio.

- Fully digital borrower experiences: Borrowers will expect a clearer self-serve experience, with access to balances, statements, payment options, loan updates, and documents without waiting on the servicing team.

For lenders still using loan servicing spreadsheets, these changes make manual servicing harder to justify as the portfolio grows.

Final Thoughts

Spreadsheets are a practical starting point for private lenders, but they become harder to rely on once servicing depends on more payments, reports, borrower updates, and investor records.

At that stage, the next move should make the servicing process easier to manage, not just easier to track. Mortgage Automator helps lenders bring origination, servicing, payments, reporting, borrower portals, and investor workflows into one connected platform, giving teams a stronger foundation for growth.

For lenders ready to replace spreadsheet-based servicing with a more scalable process, Mortgage Automator is a strong place to start. Book a demo to see how it works.

Frequently Asked Questions

What are the best alternatives to spreadsheet-based loan servicing?

For private lenders looking to scale, Mortgage Automator is the strongest option because it connects servicing with the rest of the lending process. Other alternatives to spreadsheet-based loan servicing include LoanPro, The Mortgage Office, Nortridge, TurnKey Lender, Bryt Software, and LendFoundry. The right fit depends on whether a lender needs a simple servicing upgrade, deeper customization, or a broader lending platform.

When should private lenders move from spreadsheets to software?

The move usually makes sense when the spreadsheet starts creating more work than clarity. If the team is manually reconciling payments, chasing reports, managing compliance records across files, or fielding more requests for online payments, it may be time for software.

Why do spreadsheets create servicing errors?

Loan servicing spreadsheets leave too much room for small errors to carry through the servicing process. One missed update, copied formula, outdated version, or incorrect payment entry can affect balances, reports, borrower records, and create follow-up work.

How can software reduce servicing errors and chargebacks?

Loan servicing software reduces the manual steps that often lead to payment errors. With automated tracking, ACH/PAD and autopay support, reconciliation tools, and audit trails, teams have a cleaner way to manage repayment activity and investigate chargebacks when they happen.

What features should mortgage loan servicing software for small lenders include?

At minimum, small lenders should look for software that can track payments, support ACH/PAD and autopay, give borrowers portal access, generate reports, organize documents, maintain audit logs, and support investor and compliance reporting.

Can loan servicing software replace spreadsheets completely?

In most cases, yes. Lenders may still use spreadsheets for one-off calculations or ad hoc reporting, but they should not have to rely on them as the main servicing record once dedicated software is in place.

Is Mortgage Automator suitable for small private lenders?

Yes, especially for small private lenders that are preparing to scale. Mortgage Automator helps teams manage origination, servicing, payments, reporting, borrower communication, compliance, and investor workflows in one connected platform.