“The first questions lenders ask us are almost always about reporting, compliance, and scale.”

When private lenders begin evaluating a new Loan Origination System (LOS), they aren't looking for flashy interfaces or aesthetic UI. They are looking for an escape from costly operational bottlenecks. If you manage a growing hard money or private lending fund, you already know that the manual workarounds used for your first ten loans will completely break down by your hundredth.

To build a resilient fund, your software evaluation must move past surface-level features to focus on the underlying infrastructure. The most successful operators pressure-test their technology based on three core areas of concern.

Building for Scale: Architecture Over Administration

Growth is the goal, but uncontrolled growth is a liability. Many funds attempt to solve increasing loan volume by adding administrative headcount. This linear hiring model eventually erodes profit margins and slows your speed to fund.

True scalability in private lending technology means doubling your portfolio volume without doubling your back-office staff. When reviewing a platform, look for a centralized pipeline that eliminates duplicate data entry across origination and servicing. A platform built for growth does more than store data; it uses automated workflows to trigger tasks, emails, and notifications based on loan status changes.

The Litmus Test: Ask a vendor to demonstrate the transition from 50 to 500 active loans. If the process requires manual "export-to-Excel" steps to bridge the gap, the system is simply a digital filing cabinet rather than a tool for scale.

Compliance as a Competitive Advantage

The regulatory environment for private and hard money lenders is tightening across North America. Managing compliance is no longer a localized task. It is a massive operational hurdle that requires active guardrails rather than passive storage.

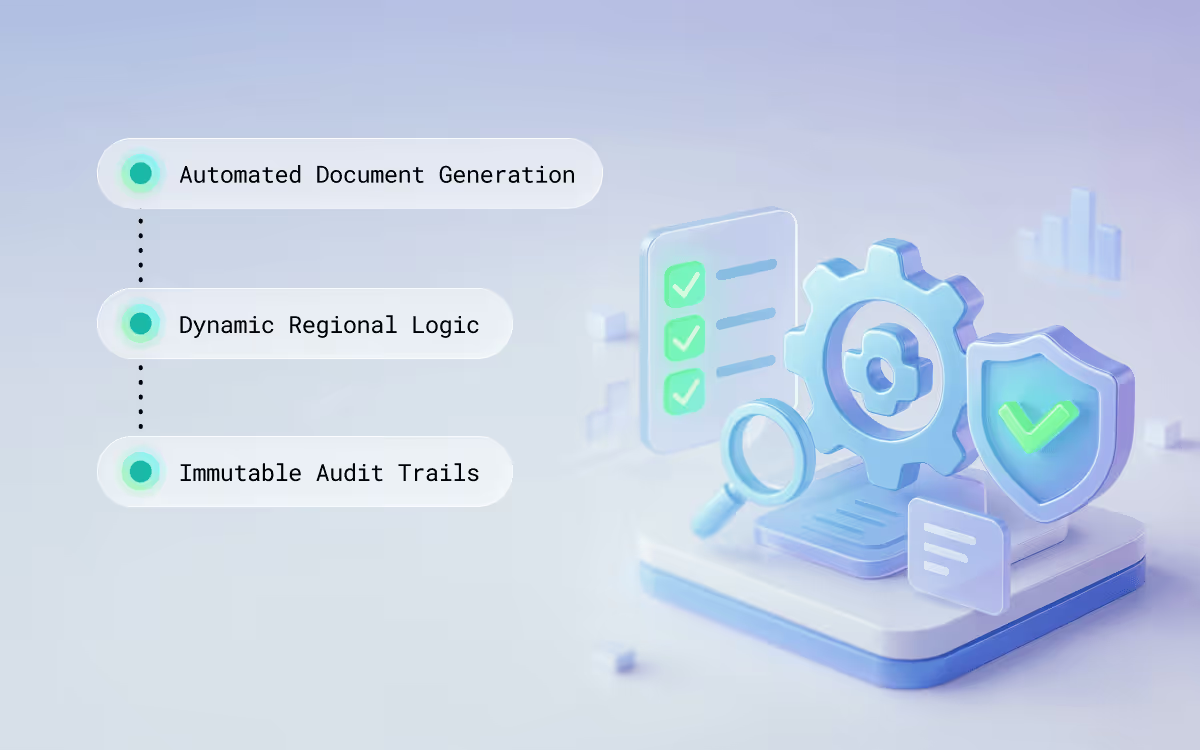

A single broken spreadsheet formula miscalculating an Annual Percentage Rate (APR) or a missed step in a borrower suitability assessment is a direct threat to your lending license. Your software should act as a silent partner in risk management through several key functions:

- Automated Document Generation: This ensures every disclosure is mathematically and legally sound before the borrower sees it.

- Dynamic Regional Logic: Systems should automatically adjust fees and disclosures based on specific state or provincial usury laws.

- Immutable Audit Trails: A digital paper trail logs every change and approval, making regulatory audits a routine check rather than a crisis.

Transparency Through Automated Reporting

You cannot manage what you cannot measure. For fund managers, the end-of-month reporting cycle is often a multi-day nightmare of pulling bank data and manually emailing statements. This manual labor drains your team's energy and introduces the risk of human error.

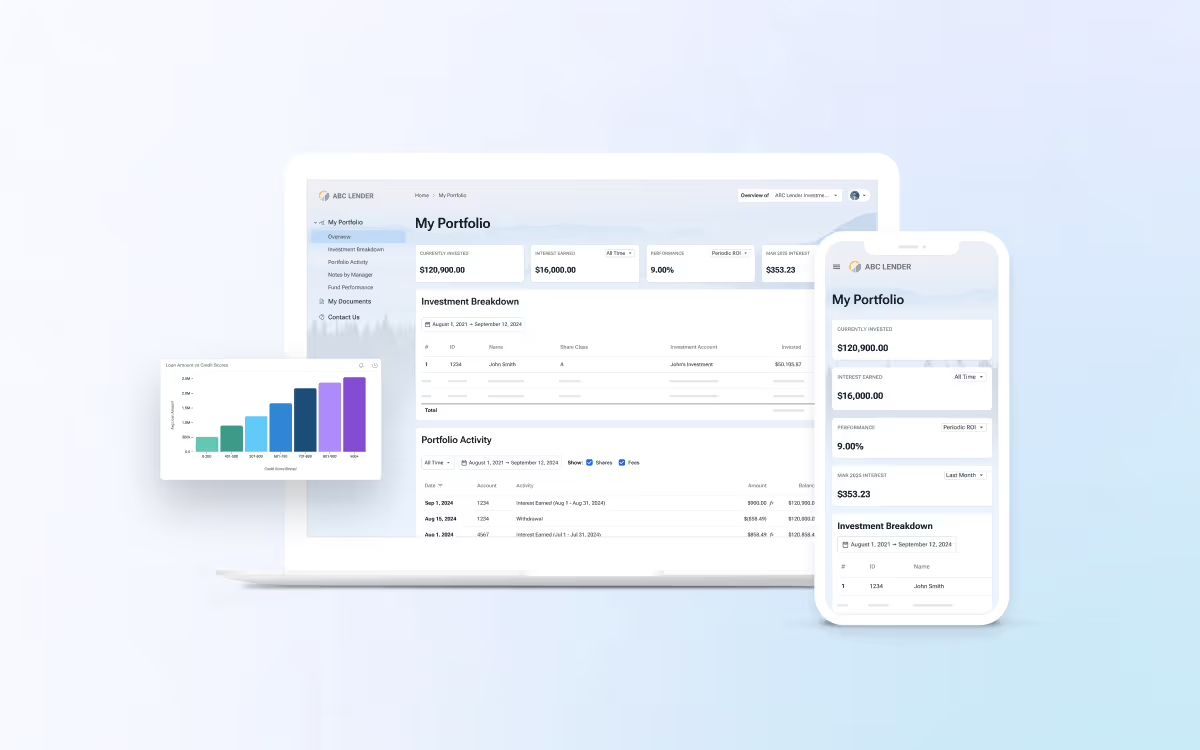

Modern hard money lending software should turn that multi-day project into an instant, real-time process. Beyond internal management, reporting is your primary tool for maintaining investor trust.

Real-time dashboards provide instant visibility into performing versus non-performing assets, while automated maturity tracking keeps your capital deployed by alerting you to approaching payoffs. Furthermore, providing investors with self-serve portals to download their own tax documents and statements builds the professional credibility required to attract institutional-grade capital.

Choosing Infrastructure for the Future

Evaluating software is about choosing the foundation for where you want to be in five years. You can have the best deal flow in the industry, but your business remains at risk if your back-office cannot handle the volume, accurately report the numbers, and stay compliant.

Look for a technology partner built to handle the heavy lifting, allowing you to stay focused on what you do best: funding the next deal.

Ready to see what a truly scalable LOS looks like?

Book a Demo to see our reporting and compliance guardrails in action!