Top 5 Takeaways from our Webinar, From 30 Loans to 300: How Private Lenders Scale High-Volume Operations.

Two private lending founders, Ryan MacNeil (Keystone Capital) and Jake Lasko (Defiance Capital), share what it takes to scale from a handful of loans to 300+:

- Know your market deeply before expanding geographically or by product.

- Build systems and document processes before you need them, not after.

- Technology like Mortgage Automator can replace administrative headcounts and build investor confidence.

- Hire for underwriting capacity first; business development can come later.

- Intentional, profitable growth beats chasing volume for its own sake.

I recently sat down with two experienced private lending operators: Ryan MacNeil, Co-Founder and President of Keystone Capital Group, and Jake Lasko, President of Defiance Capital. We had a candid, practical conversation, and I wanted to share the highlights with you here.

Both Ryan and Jake are Mortgage Automator customers who built their lending businesses from the ground up. Their paths look different on the surface, but the principles that drove their growth share a lot in common.

Know Your Market Better Than Anyone

Jake's story with Defiance Capital is a masterclass in geographic focus. Operating in Tulsa and Oklahoma City, from Colorado, no less, his team made a deliberate bet to understand a specific market deeply, rather than cast a wide net. That hyper-local knowledge became their competitive edge.

"The magic we've seen is that hyper-focus in a market," Jake told us. "Understanding that market potentially better than your clients is a huge trigger to bring that total idea of mutual success."

When COVID sent remote workers looking for affordable places to land, Defiance was already embedded in a market that was suddenly in high demand. That wasn't luck; it was the payoff of staying committed to a geography and building genuine relationships there.

Ryan's journey was different, but equally instructive. He grew up watching his family's Atlantic Canadian lending business, Graysbrook Capital, scale from a handful of loans to over 300, before selling to a credit union. When he launched Keystone Capital three years ago, he came armed with hard-won lessons about what works and what doesn't.

One of those lessons is that smaller loans in rural areas carry outsized risk because legal and enforcement costs remain fixed regardless of loan size. Keystone deliberately avoided that pitfall from day one.

Build the Infrastructure Before You Need It

One of the clearest themes of our conversation was the value of building systems before growth, not in response to it.

Ryan showed up to Keystone's launch with a 30-page business plan, a signed shareholders agreement, and Mortgage Automator already set up. "We knew we were in this business for the long term," he said. "We knew we wanted to scale. So why bother waiting until we're 10 or 25 loans in?"

Jake took a similarly intentional approach with technology. About six months into operations, he decided to bring in a proper loan management system rather than trying to manage growth with spreadsheets. "I can only imagine the number of people we would have needed to hire just to keep up with the volume we were seeing," he reflected. Having the right infrastructure meant capital could stay in loans rather than in overhead.

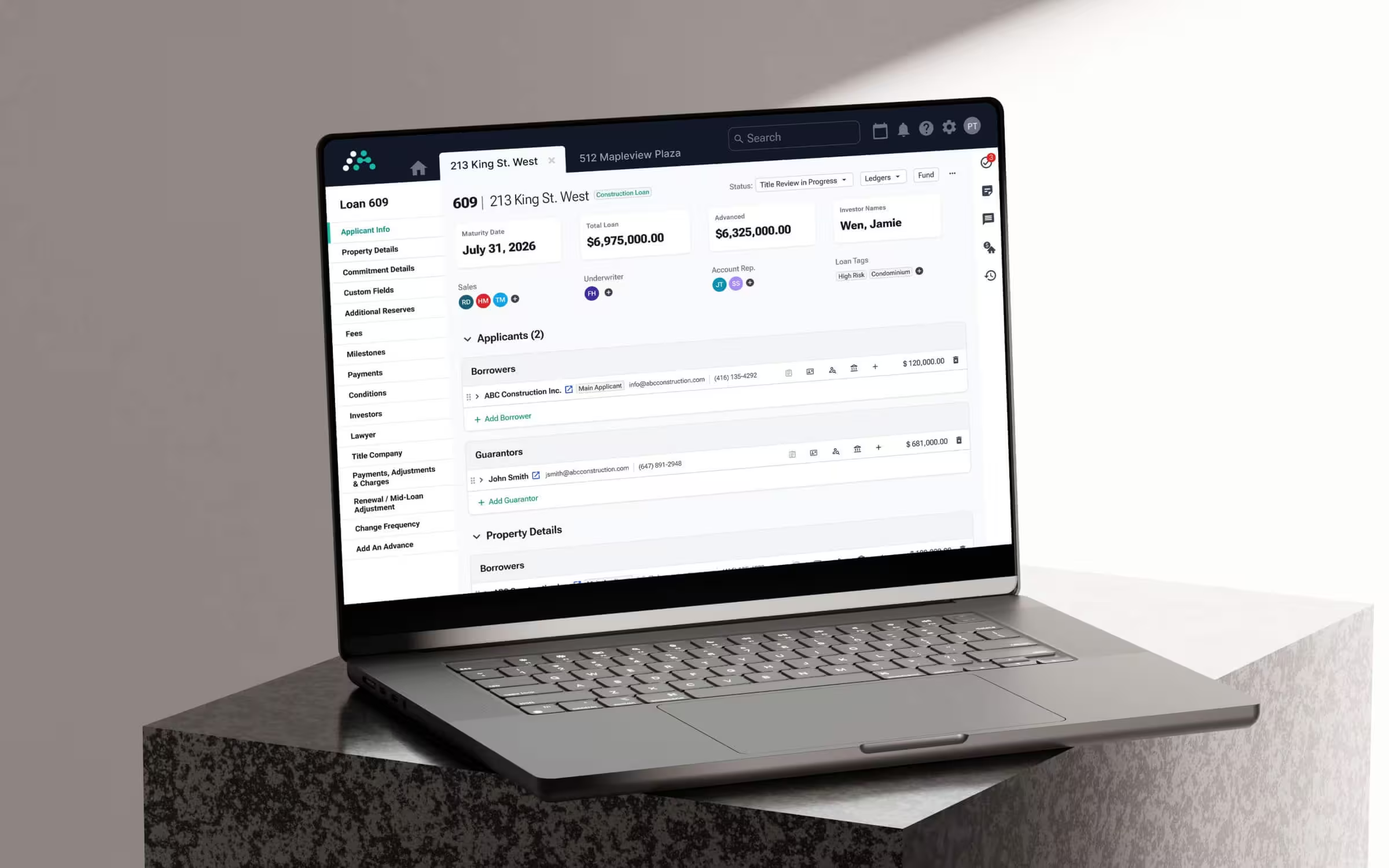

Ryan put it in terms every lender will appreciate: having Mortgage Automator in place has saved Keystone at least one or two administrative headcount positions — over $100,000 per year in salary.

Processes Are a Competitive Advantage

Both founders emphasized the importance of written, living process documentation, not just as an internal tool, but as a foundation for growth and investor confidence.

Ryan recalled joining the family business and finding a 40,000-line Excel spreadsheet tracking loans, with no formal processes documented anywhere. When the credit union acquired the business, one of the first things they did was require every process to be written down. "That was one of my biggest takeaways," Ryan said. "Keeping these evergreen, just to allow for a more seamless transition when you inevitably experience turnover."

Jake framed it from an investor perspective: being able to click print and hand someone a clean loan tape with portfolio metrics is a very different pitch than handing them a sprawling spreadsheet. Systems build credibility, and credibility raises capital.

How They Raise Capital and Win Investor Trust

Speaking of capital, both founders shared how they thought about fueling growth through outside investors, and how their systems played a direct role in that.

Defiance Capital started with a classic family-and-friends debt strategy, then formalized into a full fund after about 18 months of operating history. "We've got a substantiated business that we can now market out there," Jake explained. The fund was built around transparency and accessibility for investors, demonstrating proof of concept, clean reporting, and a genuine interest in their success.

Jake was candid that growth on the investor side was slower than expected, partly because some investors were cautious about such a geographically concentrated portfolio. But consistency helped. As the newsletter kept arriving and the fund kept hitting its targets, those who had been on the sidelines started picking up the phone.

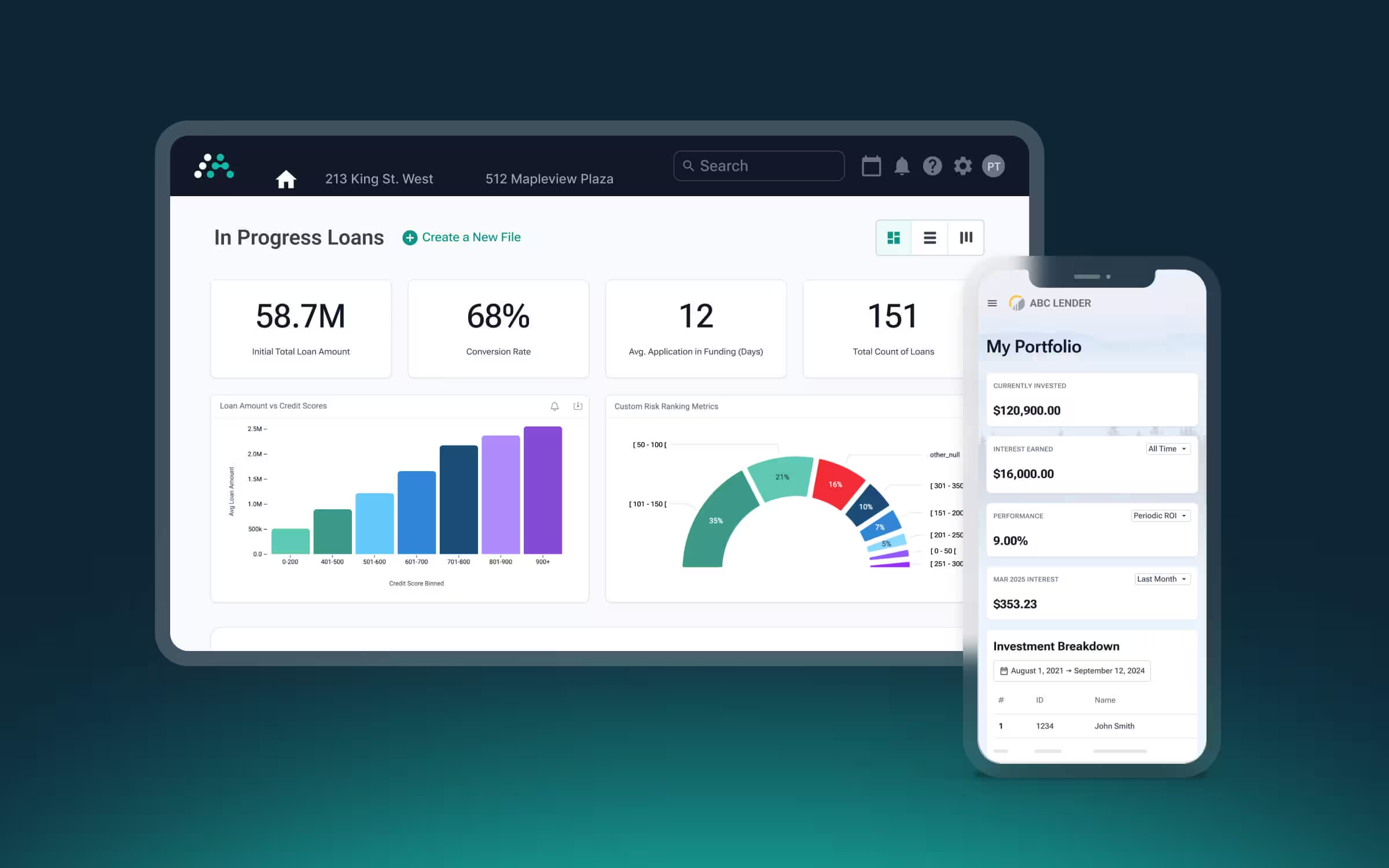

Ryan highlighted a similar dynamic at Keystone, where the MIC (Mortgage Investment Corporation) structure — Canada's equivalent of a residential mortgage fund — allowed them to scale investor capital and take on larger loans up to $2 million. In both cases, the ability to pull up a dashboard and show investors exactly where the portfolio stood, where the stress was, and what the weighted average metrics looked like made a tangible difference in building confidence.

Who to Hire First

For lenders considering when and how to grow their teams, both Ryan and Jake offered clear, consistent advice: underwriting capacity comes first.

Jake's first hire after bringing on Mortgage Automator was an additional underwriter to keep pace with deal flow and maintain the fast decision-making his clients had come to expect. From there, he added an operations and admin role focused on getting the most out of the platform by managing the client portal, organizing documentation, and ensuring nothing fell through the cracks.

Ryan's experience at Graysbrook followed a similar sequence: underwriter first, then finance manager, then admin, with business development coming last. At Keystone, he replicated that model, with one co-founder handling underwriting and risk, another focused on capital raising, and an executive assistant and a junior underwriter added as volume grew.

The throughline: revenue-generating capacity means nothing if the underwriting and operations side can't keep up. Getting that foundation right first protects both your margins and your reputation with referral partners.

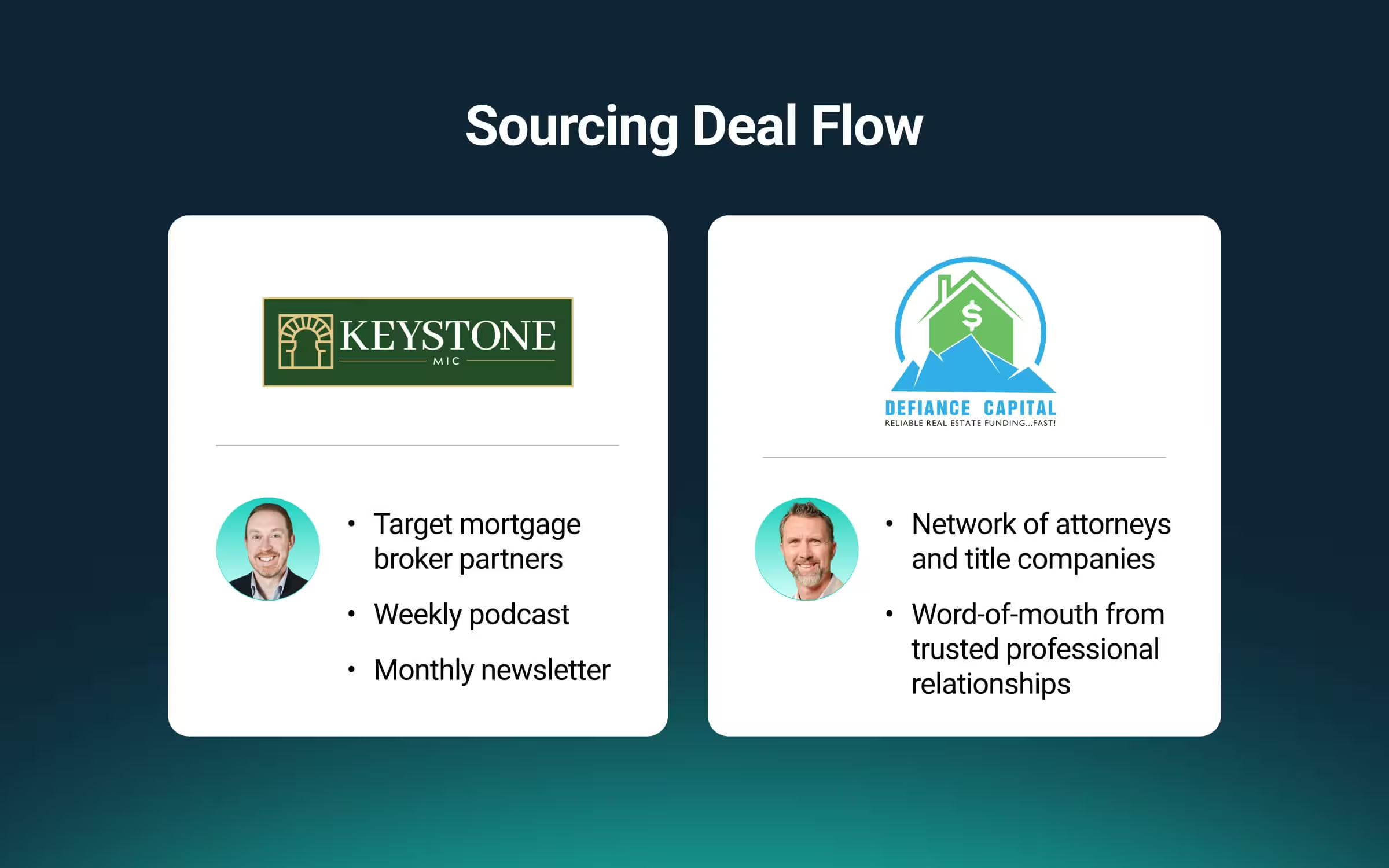

How They Source Deal Flow, Two Very Different Models

One of the more interesting contrasts in our conversation was how differently Ryan and Jake approach deal sourcing, and both are working well.

Ryan's business runs almost entirely through mortgage broker partners. At Keystone, consistent and targeted marketing to top-performing brokers has been a core strategy from day one. That includes a weekly podcast, a monthly newsletter that goes out on the first or second of every month without fail, and a deliberate focus on staying top-of-mind with the referral sources who actually drive volume. The contrast with the family business, where marketing happened when time permitted, was stark and intentional.

Jake, by contrast, has zero brokers sending him deals. His referral network is built entirely through attorneys and title companies who see Defiance show up at the closing table with funds as promised, no surprises, and clients eager to do their fifth or sixth deal. "Those sorts of stories then dive into how we've continued to grow our loan scale over time," he told us. Word-of-mouth from trusted professional relationships, earned through consistent execution, has been his engine.

Neither model is right or wrong, but both require consistency and intentionality to sustain.

Hold Your Pricing

A member of the audience asked if they had to lower fees to win more business as they scaled?

Both pushed back on the idea. Ryan acknowledged that on larger deals (a million-dollar loan), there's naturally more pushback on a 2–3% fee than on a $100K loan, and some pricing flexibility was required as average loan sizes grew. But at Keystone today, he's held pricing firm. "We do lose out on some loans to competition. But we're still making strong margins. We're going to do it strategically and not just give away on pricing to achieve scale."

Jake took a nuanced approach: rather than across-the-board discounting, he gets more dynamic with pricing for loyal clients based on track record, geography, and property liquidity. It's a retention tool, not a race to the bottom. And it helps combat competitors who try to undercut on price to poach established relationships.

What Didn't Work: Lessons From the Misses

No scaling story is complete without an honest accounting of what didn't go as planned.

Ryan's most instructive miss was an attempted expansion into Ontario after Graysbrook was acquired by the credit union. Ontario is Canada's largest and most competitive private lending market, and the expansion never gained the traction they'd hoped for. In hindsight, he attributed it to a lack of consistent local presence — no permanent boots on the ground — combined with limited market-specific knowledge and the challenge of differentiating in a market full of established players charging lower rates. The lesson: market knowledge and local relationships aren't things you can build remotely or on conference trips alone.

Jake faced a similar challenge operating outside his core market, though his challenges were more operational in nature. Running a business from Colorado while lending in Oklahoma created real staffing constraints. Not enough local talent, and the added complexity of managing remote employees across processes that were still being built. He's navigated it but has acknowledged that it required more intentionality around remote workflows than he initially anticipated.

Both also noted that success attracts imitation. When you carve out a niche and make it work, copycats follow. The best defense, they agreed, is staying true to your process, your relationships, and the standards that made you credible in the first place.

Scale Intentionally, Or Don't Scale at All

Perhaps the most refreshing moment of the conversation was Ryan's direct question to anyone considering growth: Do you actually want to scale?

"Growing your book is great. But if you're making the same bottom line at $300 million that you were at $50 million, and you're adding all this staff and complexity, is this really the strategy you want?" It's a question worth sitting with. Sometimes, staying focused and profitable at a comfortable volume is exactly the right answer.

Jake echoed this with his own version: stay nimble, but don't confuse nimble with reactive. Trusting your existing clients to guide measured expansion into new geographies and loan types is very different from chasing every opportunity that appears.

The common thread across Ryan and Jake's journeys is that intentional operators build durable businesses. They knew their markets, documented their processes, invested in the right tools early, held the line on pricing, and stayed true to the principles that made them credible in the first place.

If you're mapping out your path from 30 to 300, the webinar replay is worth your time to watch. I hope their stories give you both inspiration and a practical framework to build from.

Want to see how Mortgage Automator helps private lenders scale with confidence? Reach out to our team — we'd love to show you around.